Enterprise management incentive replacement options

Enterprise management incentive (EMI) options are the most popular tax advantaged share option scheme available to private limited companies and for good reason. Published in Taxation on 22nd March 2022, written by Nick Wright.

They allow the company to reward and incentivise its employees with no tax charges at either the grant or exercise of the options, as long as the qualifying conditions are met. So, the employee pays capital gains tax only when they sell the shares.

There are also relaxations to the business asset disposal relief (BADR) conditions for EMI option holders, such as the removal of the personal company requirement. This means individuals do not need to hold the minimum 5% ownership for the previous two years and the time the options are held may be included within the two-year holding period requirement.

However, there are several disqualifying events that may trigger an income tax charge if the options are not exercised within 90 days of the aforementioned disqualifying event.

- Disqualifying events are outlined in ITEPA 2003, s 534 to s 537 and include:

- the company becoming a 51% subsidiary of another;

- the company no longer meeting the trading activities requirement;

- the employee ceases to be eligible, eg they resign or cease to meet the minimum qualifying hours; and

- there is an alteration of the company’s share capital which changes the value of the shares.

Dealing with company reorganisations, many proposals will trigger these disqualifying events, such as capital reduction demergers requiring the insertion of a new holding company, share-for-share exchange transactions and outright sales.

It is often the case in company sales that the purchaser will not intend the EMI option to remain in place; options are often exercised pre-sale allowing the option holder to share in the proceeds of the sale.

However, for company reorganisations that are carried out for genuine commercial purposes and when the existing shareholders and management team remain in place, the disqualification of the existing EMI options will often be an unfortunate and unintended consequence of the wider planning.

It is for this reason that Part 6 of Sch 5 in ITEPA 2003 provides for such circumstances which may often be used to retain the EMI status of the options by replacing them with options in the new holding company and thus ensuring they remain qualifying.

What transactions qualify?

For the purpose of the replacement option provisions, there is a ‘company reorganisation’ when a company obtains control of the company with unexercised options (for the remainder of this article this company will be referred to as the ‘EMI company’) by:

- a general offer to the company as a whole;

- a general offer for the class of shares over which the unexercised options are held;

- a court sanction compromise agreement;

- minority shareholders exercising ‘tag-along rights’; and

- obtaining all the shares of the company as a result of a qualifying exchange of shares.

Note that the first two bullets exclude shares already held by the prospective purchaser or a person connected to them, ie the general offer is made to everyone other than the acquiring company and their connected persons.

A general offer is one that is made in writing to all shareholders – or all shareholders of the relevant class – with a fixed time limit for shareholders to respond. While it is made to all shareholders, it does not necessarily have to be by the same means – minority shareholders may receive a summary document while majorities receive a detailed document outlining the proposals.

It should also be noted that there are a couple of other scenarios in relation to EMI shares that may be relevant in the event of the EMI company being acquired:

- Where the acquiring company does not offer replacement options, the options must be exercised within 90 days of the acquiring company obtaining control in order to preserve the tax benefits.

- Where the options have already been exercised by the date the acquiring company obtains control, assuming the option holder (now shareholder) is provided with shares in the acquiring company as part of the transaction, those new shares continue to be treated as EMI shares and continue to retain the benefits for BADR purposes.

Qualifying exchange of shares

So, in practice, a company sale or an exchange of securities are common transactions where we may consider the granting of replacement options.

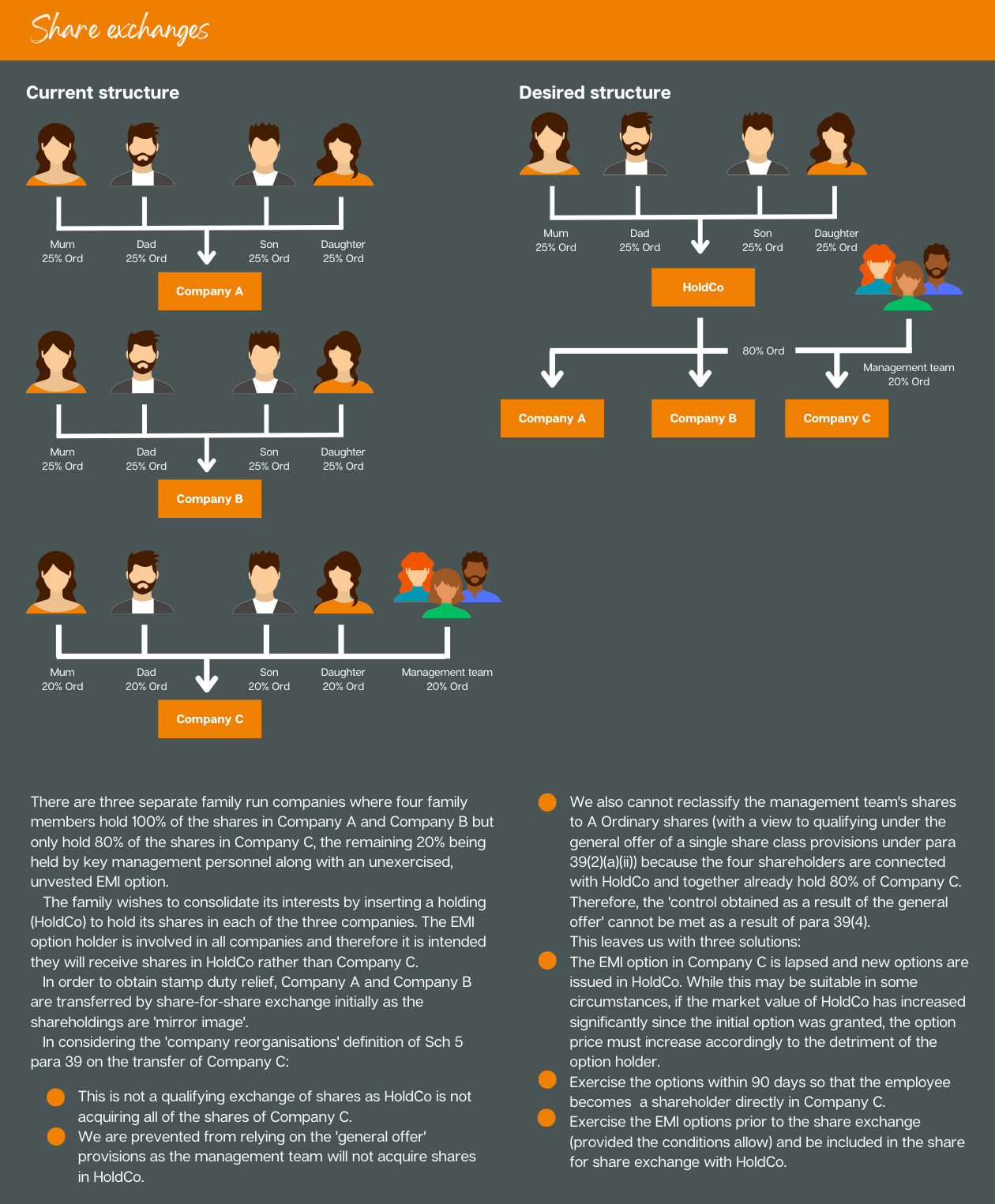

The legislation clearly states that, in the case of share exchanges, the acquiring company must obtain all the shares of the EMI company for the replacement options provisions to be available; see Share exchanges.

Further, the consideration must be wholly in the form of new shares and those shares must have equivalent rights to the original shares and be in the same proportion to the shareholders’ original shares. The share-for-share exchange must be a ‘mirror image’, except that the acquiring company may also have in-issue subscriber shares or other shares issued in previous share for share exchanges.

As the consideration must be wholly in the form of new shares, this prevents most management buyouts from qualifying under this provision and we must then consider the ‘general offer’ provisions instead.

Other conditions that must be met are that the exchange must be for bona fide commercial reasons for which HMRC will provide clearance under TCGA 1992, s 137.

Replacement options

ITEPA 2003, Sch 5 paras 41 to 43 contain the provisions for the replacement option itself. The first condition is that the option holder must release their rights over the existing option in exchange for new options with equivalent rights but in the acquiring company.

There are a couple of points to note here. First, the acquiring company is under no obligation to offer replacement options, as this is at their discretion. Second, the replacement options must be granted within six months of the acquiring company obtaining control.

In relation to the acquiring company, it must:

- meet the independence test, ie not be controlled by another company; and

- meet the trading activities test.

In relation to the employee, the conditions of Sch 5 Part 4 continue to apply:

- They must continue to be employed by the acquiring company or a member of their group.

- They must work at least 25 hours a week or, if less, 75% of their working time whether in an employed or self-employed capacity.

- The employee, together with their associates, cannot hold a material interest in the company (including a company within the group). A material interest being more than 30% of the ordinary share capital, either directly or via beneficial interests.

Note, in its Employee Tax Advantaged Share Scheme User Manual, para ETASSUM55030, HMRC states that it believes a new working time declaration should be completed when the replacement options are issued.

In relation to the replacement options, the conditions are:

- They must be granted for the purpose of retaining the employee within the company or group and not as part of a scheme where one of the main purposes are to avoid tax.

- The type of shares that may be acquired must be fully paid up, non-redeemable, ordinary shares.

- The options must continue to be exercisable within ten years of the date the original options were granted.

- The terms must be agreed in writing.

- The terms of the options cannot be assigned to anyone other than the option holder.

- The total value of shares covered by unexercised qualifying options in the acquiring company must not exceed £3m. For this purpose, the value of shares subject to the replacement option is taken to be the same as the value of shares under the original option immediately before the options are replaced. This may be particularly relevant in cases where the acquiring company already has EMI options in issue.

There are two key elements to the replacement option values. First, the total market value of the shares under the old options must be equal to the total market value of the shares under the new options immediately after they are replaced.

Second, the total amount payable for the shares under the new option must be equal to the total amount that would have been payable for the acquisition of shares under the old option.

It is also worth noting that these conditions must be met at the time the options are replaced, not when the reorganisation takes place. For example, there may be a circumstance when the acquiring company completes the reorganisation, issues EMI options to existing employees, say, three months later worth £2m and then grants the replacement options. If those replacement options are worth more than £1m, the conditions are failed.

Finally, HMRC must be notified within 92 days of the grant of any new or replacement options.

Consequences of a replacement option

If the above conditions are met, there will not be a disqualifying event and the qualifying EMI options will retain their benefits in the acquiring company. In addition, much like the share-for-share provisions, the new option is treated as if it was granted on the date of the original option. So, for the purposes of BADR, the holding period of the original option may be taken into account.

There are two notable conditions missing from the above in relation to the acquiring company, namely they do not need to satisfy the £30m gross assets or the 250 full-time employee tests. So, even if large companies are acquiring the EMI company, this does not necessarily prevent the replacement option conditions from being satisfied.

Calculating the number and value of options

As outlined above, there are several clauses dictating the value and number of shares to be subject to the option, specifically:

- The total market value of shares under option must be the same immediately after they are replaced.

- The total amount payable for the shares under option must be unchanged.

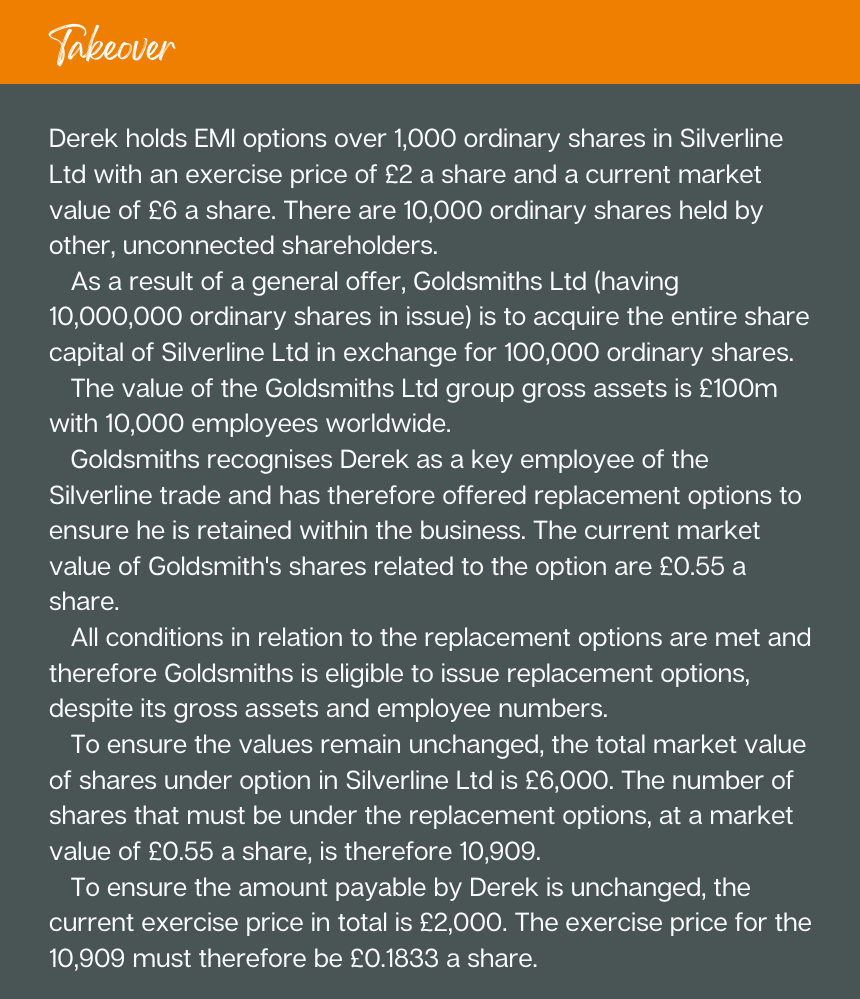

In practice, it is likely that the number of shares in issue in the acquiring company will differ from the original company. Therefore, we need to consider the value of both companies at the time of the transaction; see Takeover.

Conclusion

The conditions for entitlement to issue replacement options have been outlined above and the key point to make is that the normal EMI conditions must continue to be met for the replacement options. The main exceptions are that the acquiring company does not need to satisfy the £30m gross assets, nor the 250 full-time employee tests. The amount payable for the shares under option must remain unchanged and the value of the shares under option must also be unaffected, so it is therefore beneficial to seek approval from the HMRC shares and assets valuation team as part of the process.

Certainly, the existence of EMI options in a company must be a key consideration in any tax planning undertaken for clients. However, in the vast majority of cases where transactions are undertaken for commercial purposes, it is often possible to ensure that company reorganisations can be facilitated without triggering a disqualifying event.

The vital point is to ensure those conditions are satisfied and the time limits set out above adhered to, both in terms of issuing the new options and in notifying HMRC.

Identifying and outlining these issues early is important, given that additional work will be required, in particular from a legal perspective in drafting the paperwork and also from the adviser in valuing the companies and ensuring the qualifying conditions are met.

Nick Wright

This email address is being protected from spambots. You need JavaScript enabled to view it.

07891 203889

Published in Taxation on 22nd March 2022, written by Nick Wright.

https://www.taxation.co.uk/articles/enterprise-management-incentive-replacement-options