Accounting for share exchange transactions

Published in Taxation on 15th August 2022.

An area not necessarily at the forefront of every tax adviser’s mind when designing company restructure transactions is how the proposals will impact the accounts of the companies subject to the restructuring.

Whilst it may be easy to consider this the remit of the company’s accountant (if different), the commercial impact on the accounts should not be overlooked, as in some cases an adverse accounting outcome may jeopardise the entire purpose of the restructuring, such as in cases where reserves are substantially reduced before a sale.

The effect on distributable reserves is always an important point in ensuring a successful transaction. Another, sometimes misunderstood, concept is the accounting for share exchange transactions and the effect of Chapter 7 of Companies Act 2006. The effect of which may, in turn, impact on the ability to creates reserves via a reduction of capital.

In particular, the requirements of s.612 that, in many transactions, any ‘premium’ is to be taken to a merger relief reserve rather than share premium account.

The correct treatment

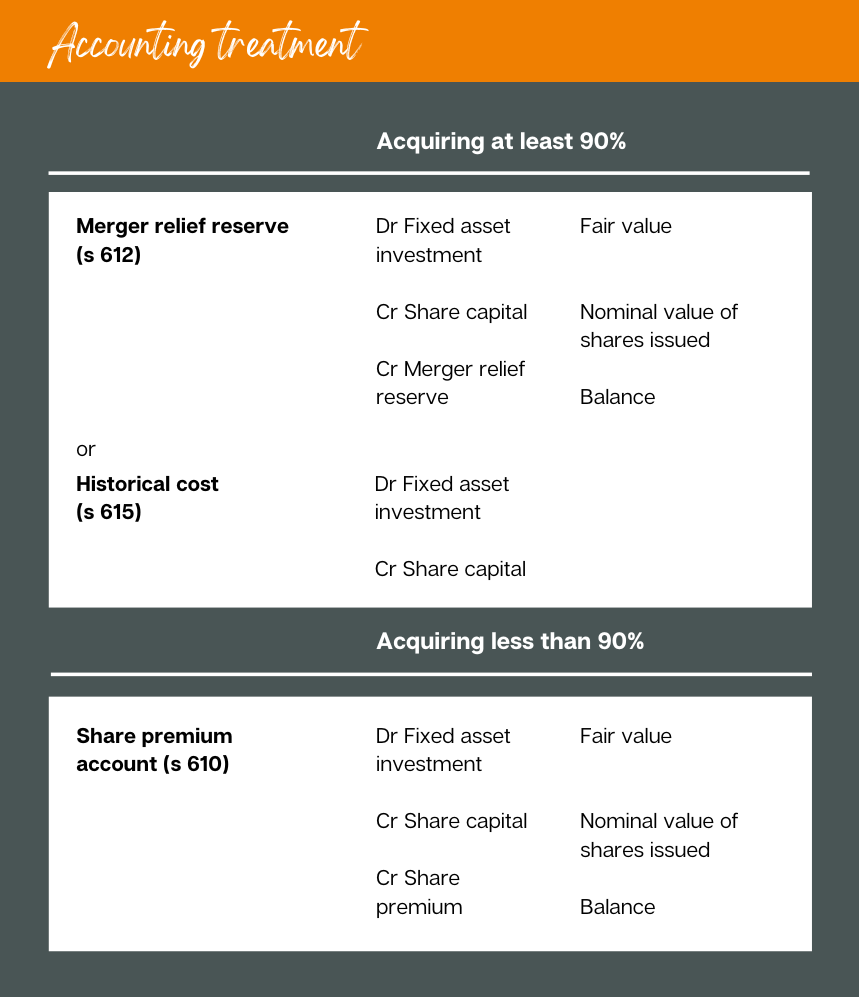

Generally, the starting point where a company issues shares at a premium, is that the nominal value of the shares issued is credited to the share capital account and the excess of fair value over nominal value is credited to the share premium account, this is in accordance with CA 2006 s.610.

However, s.610 is subject to certain other provisions, namely s.612 (merger relief), the application of which will be dependant on whether or not at least 90% of the share capital of the target company is being acquired.

Acquiring at least 90% of target

In the common circumstance of inserting a new holding company (‘HoldCo’) above the existing company or group, HoldCo acquires 100% of the share capital of target meaning s.612 is relevant.

In fact, s.612 applies to any circumstance where at least 90% of target is acquired as a consequence of the transaction.

s.613 provides more detail about exactly what this means, though essentially if HoldCo acquires at least 90% of the nominal value of target’s equity share capital (excluding shares held in treasury) the conditions are met.

If target has different classes of shares in issue, the conditions must be met in relation to each of those classes of shares taken separately.

It is also worth noting that shares held by any other group companies of HoldCo are included in considering this 90% limit.

s.612 provides ‘merger relief’, (not to be confused with merger accounting which is an entirely separate concept) whereby s.610 is disapplied and instead of the excess fair value over the nominal value of shares issued being taken to the share premium account, it is posted to a merger relief reserve.

It would seem to me that, suggesting s.612 provides ‘relief’ from the creation of a share premium account, is a little misleading because:

a) if the company acquires at least 90% of the share capital and wishes to state the investment at fair value, it must be posted to the merger relief reserve, the share premium account is not an option, and

b) it can complicate matters when it comes to unlocking distributable reserves (see below).

However, where the circumstances to which s.612 apply (i.e. the acquiring company acquires at least 90% of the share capital of target) the company does have the option of stating the investment at fair value, as above, or stating it at cost (by virtue of s.615) i.e. the nominal value of shares issued is debited to fixed asset investments and credited to share capital.

Generally, companies wish to show a strengthened balance sheet and therefore opt to recognise the investment at fair value however it is not unknown for the cost option to be applied.

Acquiring less than 90% of target

Where HoldCo acquires less than 90% of the shares in target, s.610 requires the fair value in excess of the nominal value of shares issued to be recognised within the share premium account.

There is no ‘relief’ in these circumstances.

The accounting treatment may be summarised as follows.

Why does it matter?

Take, for example, two trading companies, each owned seperately by two siblings. There are significant synergies between the businesses and it is felt that the companies being held within the same group will be commercially beneficial.

The first sibling holds 100 Ordinary £1 shares in Company A and it has been agreed that Company A will acquire the entire share capital of Company B in exchange for a new issue of 100 Ordinary £1 shares to the second sibling.

The result being that Company B will be a wholly owned subsidiary of Company A and the siblings hold 50% of the share capital of Company A each.

At some point in the future, a distribution is proposed from Company A but there are insufficient distributable reserves for a lawful distribution to be made.

It is therefore proposed to reduce Company A’s share capital by the ‘premium’ initially recognised on the original share exchange transaction.

However, the accountant incorrectly treated the ‘premium’ as share premium and the solicitor has relied on this information in preparing the capital reduction documentation.

As the share premium was never a ‘share premium’ the consequent capital reduction was ineffective and the distribution by the company was therefore unlawful.

How do we resolve the issue?

As outlined above, the correct treatment of the original share exchange transaction was that the fair value of Company B (less the £100 nominal value) should have been recognised as a merger relief reserve.

Whilst the recognition of the merger relief reserve means a capital reduction cannot be made against this reserve in the first instance, a few additional steps should resolve this. Specifically, a bonus issue of shares would be made against the merger relief reserve in order to convert it into share capital.

Having converted the merger relief reserve into share capital a capital reduction may lawfully be made by the company.

The main issue the directors should be aware of when undertaking such a transaction is that they will be required to sign a solvency statement that the company is a going concern.

A relatively straightforward solution but an important distinction in order to ensure no future issues arise e.g. in the event of a future sale and the due diligence of the buyer.

Alternatively, depending on the circumstances, it may be possible for the nominal value of shares issued as part of the share exchange transaction to be equal to the fair value of target, thus negating the need for either a share premium or merger relief reserve.

As to whether this is viable may vary depending on other factors of the transaction e.g. in the above example, sibling 1 only held 100 shares, sibling 2 obtaining anything other than 100 shares would have resulted in the desired 50:50 holding failing.

Conclusion

As tax advisers our main concern is with ensuring the relevant conditions within the taxes legislation is met when restructuring a company.

However, particularly where a share exchange transaction is a pre-curser to a future sale, understanding the accounting treatment will be imperative in ensuring no adverse consequences arise down the line with the effect on distributable reserves generally being a primary factor.

Provided this is both understood and considered early on there are usually mechanisms with which to ensure the desired outcome is achieved in relation to the capital and reserves of the company.

Nick Wright

This email address is being protected from spambots. You need JavaScript enabled to view it.

07891 203889

Published in Taxation on 22nd March 2022, written by Nick Wright.

https://www.taxation.co.uk/articles/accounting-for-share-exchange-transactions